The investing advice for the average American assumes the following:

- You will work and invest for 45 years, retire at 65, and live off of your portfolio (and social security) for 25 years or so.

This means that total return during the portfolio accumulation phase is the number one priority because the savings rate is low and the time horizon is very long.

The FIRE community has a very different financial picture:

- You will work and invest for 10-20 years (or less) and live off of your portfolio (with a much lower contribution from social security) for 50 years or more.

As I have stated before, at high savings rates, portfolio return doesn’t matter as much during the accumulation phase. Volatility is much more important for people with high savings rates and short investing horizons. Additionally, the portfolio distribution phase is much longer for someone pursuing FIRE, potentially 50 years or more, which again emphasizes the importance of low portfolio volatility.

A Historical Example

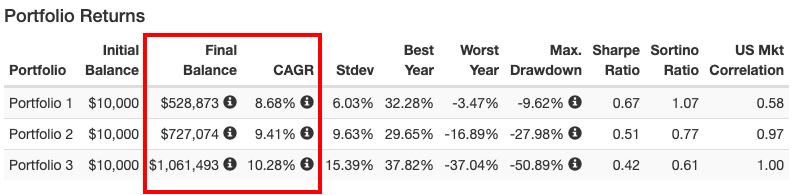

Let’s assume you are an early adopter of FIRE and want to retire at the age of 35 in 1972 (that makes you 82 today). A genie from 2019 visits you and gives you the total returns for three portfolios given an initial $10,000 investment in 1972, below:

- Portfolio 1: 20% small-cap value, 80% intermediate-term Treasury notes (IT)

- Portfolio 2: 60% total US stock market (TSM), 40% IT

- Portfolio 3: 100% TSM

Usually what people do is focus on the columns in red. Each of the portfolios has a respectable return over 8%, but Portfolio 3 ends up with almost double the balance as Portfolio 1 with an annual compound return of over 10%.

If you had to pick a portfolio to support your retirement living expenses, which would you pick?

Most people would pick Portfolio 3. It has the highest return, which is what we want, right?

No, volatility matters! Look at the “Stdev” column, which is a common measure of portfolio volatility (lower is better). Portfolio 1 has 60% less volatility than Portfolio 3, with a compounded annual return only about 15% less. It also has a higher Sharpe ratio, which is a measure of risk-adjusted return (higher is better). The Sortino ratio is a modified version of the Sharpe ratio that penalizes downside volatility more than upside volatility (again, a higher number is better).

Volatility matters because it tells us how likely a portfolio is to lose value. When you are in the accumulation phase, losing value doesn’t matter because you aren’t selling when the market falls, you continue to add money to the portfolio. During the distribution phase, however, losing value does matter because you have to withdraw money regularly to fund your living expenses. You are forced to “sell low” during distribution, and someone pursuing FIRE has a much shorter accumulation phase and a much longer distribution phase.

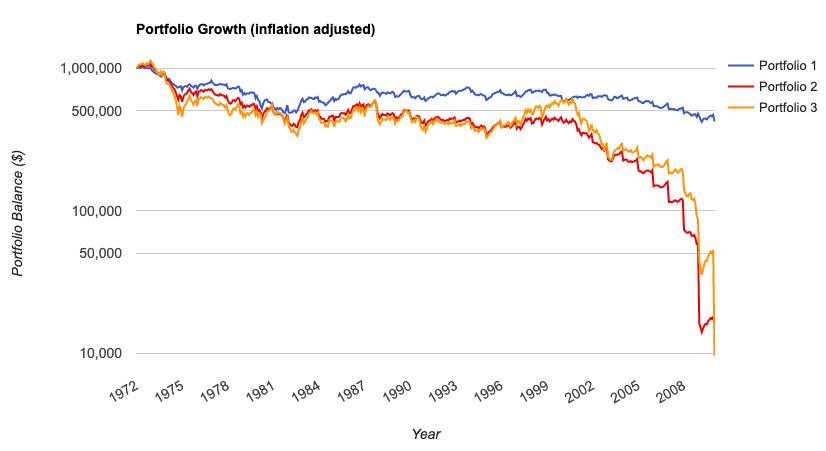

What would have happened to our 1972 retiree if they decided, looking at the future returns of their portfolio, that they would be conservative and withdraw an initial 4.5% of their portfolio balance (less than half of the compounded annual growth rate of portfolios 2 and 3) and increase it every year for inflation? Here’s the chart:

Uh oh. By 2009, Portfolios 2 and 3 are out of money, while Portfolio 1 has a portfolio balance of $421k in inflation-adjusted dollars (link to backtest). Portfolio 1 does much better than Portfolios 2 and 3, though it does get close to running out of money in 2019, with an inflation-adjusted balance of only $125k (link to backtest), but it did last a decade longer than the other two portfolios with a higher rate of return.

Volatility Matters

The point is to demonstrate that portfolio volatility matters during distribution, which is very long for someone pursuing FIRE. FIRE portfolios will likely have to endure many bear markets, and protecting against downside volatility is more important than achieving the highest possible total return.

The point is not to recommend a 20/80 SCV/IT asset allocation. The backtest has the benefit of hindsight, where we know that small-cap value was among the best-performing asset classes from 1972-2019. That asset allocation was simply chosen in order to construct a low-volatility portfolio with decent returns. It is impossible to know if small cap value will have the best returns going forward.

Withdrawal Rate Matters

Admittedly, the withdrawal rate was quite high at 4.5%, but that was simply to demonstrate that total return cannot compensate for high volatility during distribution. Another way to guard against portfolio volatility and sequence of returns risk is to lower your withdrawal rate. A withdrawal rate of 3% is not 1.5% lower than 4.5%. It is 33% lower. Instead of withdrawing $45k from a $1 million portfolio, you would only withdraw $30,000. All three portfolios survive a 3% withdrawal rate, and the highest balance is gained using Portfolio 3, though it was an extremely bumpy ride, and a deep bear market could move Portfolio 1 back into the lead (of course, if you need to sustain a $45k annual withdrawal at 3%, the portfolio will have to be $1.5 million and not $1 million for a 4.5% withdrawal rate).

Do You Have Thoughts?

Send me a Letter to the Editor via email.

I’ve decided I don’t want a comments section, but I do want feedback. The best Letters will be published on this site (with your consent, of course). I can publish anonymously or I can include your name and a backlink, whatever works for you.